Banking

Loan write-offs shoot up

Banks' written-off loans last year more than doubled year-on-year, as banks looked to bring down their default loan portfolio and clean up their balance sheet.

In 2013, banks wrote off loan amounting Tk 6,893 crore, in contrast to Tk 2,992 crore in 2012, according to central bank statistics.

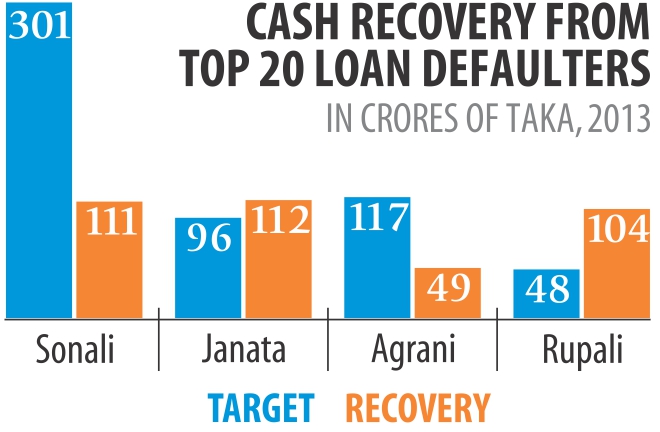

The state-owned commercial banks alone accounted for Tk 4,573 crore of the write-offs, up 288 percent year-on-year. Sonali wrote off Tk 2,177 crore, Agrani Tk 1,313 crore and Janata Tk 1,083 crore. Rupali Bank did not write-off any

loan in 2013.

As for the Tk 2,320 crore written off by private banks, four banks alone made up half of the amount.

Meanwhile, a high official of Janata Bank said the loan write-offs in 2013, which was an increase of almost 275 percent over the previous year's, does not reflect the true picture.

Loans are usually written-off at the end of the year, and the state-owned bank did not have a functioning board in the last three months of 2012. As a result, mass write-offs had to be done in 2013 to make up for the previous year's.

Efforts to recover the amount though are ongoing, he said. Last year, the bank recovered Tk 130 crore, which went directly to their income.

A high official of Sonali Bank echoed the same, adding that the bank recovered Tk 436 crore from the written-off loans in the last three years.

The practice of writing off loans started in 2003, with Tk 30,728 crore loans written off until December 31 last year. Banks make provisioning against the amount, and when the loans are recovered they boost the income and profitability.

Atiur for socially responsible financing

He emphasized that higher access to finance enhances social and economic stability.

Bangladesh Bank Governor Atiur Rahman has urged financial regulators to focus on financial inclusion including micro-insurance, micro-finance and socially responsible financing (SRF) for ensuring economic stability.

Addressing the 24th meeting of the Council and the 12th General Assembly of Islamic Financial Services Board (IFSB) in Brunei Darussalam yesterday, he made the call saying that financial inclusion and SRF would not only for improving the condition of the disadvantaged, but also for wider objective of achieving financial stability.

He emphasized that higher access to finance enhances social and economic stability, reports BSS.

Islamic Development Bank (IDB) president, governor of Sudan and chairman of Financial Supervision Authority of Indonesia supported Dr. Rahman’s views on micro-finance including Islamic micro-finance, according to a BB press release issued here.

Dr. Rahman also suggested IFSB to do more research and advocacy on capacity building of different central banks on their regulatory and supervisory role related to Islamic financing.

In addition to attending the Council meeting, the BB governor participated in the annual general meeting and a public lecture on financial stability.

News:Daily Sun/29-Mar-2014BKB to organize Halkhata 1421

Bangladesh Krishi Bank (BKB) is going to observe ‘Shubho Halkhata-1421’ with a view to expediting all types of banking activities including disbursement and recovery of loans and deposit mobilisation.

The bank will arrange ‘Shuvo Halkhata Programme-1421’ on April 13 next, marking the Bengali New Year.

All the branches of the bank will be decorated with coloured paper and leaflets will be distributed on this occasion.

In this context, the bank will chalk out a special business development programme from 6 to 24 April, 2014, being conducted at all branches of the bank across the country.

Meanwhile, high officials of the bank have been deputed to the field offices in order to conduct the programme successfully, the release said.

On the occasion, the bank will offer various activities to its customers for developing cordial relation between bank and customers.

Rupali Bank suggested for disbursing more credits

Banking sector experts advised that the state-owned Rupali Bank Limited should disburse more credit and advances to prospective borrowers in a bid to avert any long-term crisis.

They also advised the bank authority for attracting prospective entrepreneurs for taking loans from the bank.

They feared that the bank will face long-term crisis if its rate of loan disbursement slows down.

To make-up the banks’ growing costs for paying interests against higher deposits as well as increased salaries for new recruitment and also for expanding network by opening new branches, there is no alternative but to sanction new loans among potential borrowers, experts opined.

The credit growth of Rupali Bnak was 14.90 percent in December 2012 while in 2010 and 2011, the rate were 15.71 percent and 16.01 percent respectively.

In an official order in May 2013, the Bangladesh Bank limited the bank’s credit growth to 10 percent from previous rate of 15 percent. Later on September last year, the central bank, in a letter, advised the bank to reduce credit growth to 2.50 percent (on quarterly basis).

Senior banking sector experts recommend that the government should allocate the budget for credit disbursement by any bank ahead of the beginning of the year because the bank’s loan distribution activities are operated on the basis of field level target.

Besides missing the yearly credit disbursement target, then banks fail to fulfill the quarterly disbursement targets, they said adding, the similar problem arouse in case of Rupali Bank.

As a result, the banks’ credit marked a 13 percent growth, though it was set 10 percent by Bangladesh Bank.

The bank failed to maintain the central bank’s ceiling as the Bangladesh bank order was issued lately, they said.

M. Farid Uddin, Managing Director of Rupali Bank Limited said the total deposit of Rupali Bank stands at Tk 17,795 crore till December 2013 while its loans and advances amounts Tk 10,742 crore.

He said credit deposit ratio (CDR) is 60.37 percent but it needs 81 percent CDR for operating day-to-day banking activities. To maintain the level of CDR, the bank should raise its credit growth.

He also said, the bank paid Tk 13.50 crore interests on deposits, while its operating expenditure was Tk 473.55 crore, cash adjustment of goodwill value was Tk 241.73 crore. With these, the bank’s total expenditure totaled Tk 2,065.28 crore in the year.

There is no alternative to disburse more credits for making profits in order to meet the budget requirement, deducting Tk 660.79 corer incomes from total expenditure.

The credit of Rupali Bank grew in 2012 as non-funded liabilities of some reputed customers against letter of credit (L/C) turned into funded liabilities for non-compliance.

As a result, a forced loan amounting to Tk 708 crore was created. For the forced loan amount and also for increased interest payments against credit accounts resulted in huge credit balance, enhancing credit growth as well.

Sources also said that entire credit balance is not newly-sanctioned advances.

News:Daily Sun/28-Mar-2014

BB gives banks directives for operating agent banking

Bangladesh Bank (BB) has given banks some directives for operating agent banking in a safe and secure manner, reports In a circular today, the Banking Regulation and Policy Department of the central bank said every agent have a current account with the bank concerned where maximum available deposit will be Taka 1.0 million.

A customer can deposit or withdraw maximum Taka 25,000 in cash each time and such withdrawal and can be made maximum twice in a single day. This ceiling will not be applicable in case of withdrawal of inward remittance.

No “bank related people” will be appointed as agent and agent banking will have to be conducted in area (out of the preview of metropolitan city corporation and pourashava). Shariah- based banks can only conduct Islami banking at agent Money to be transacted up to customer level will have to be brought under insurance coverage, it Banks must submit some documents: a) sample copy of agreement to be signed with agents, b) plan about agent banking (including business continuity plan) and c) guidelines approved by the board of

directors about agent BB’s respective departments will give banks approval letters under which banks will be able to appoint as per its policy. For supervising the agent banking operation, the list of agents and copies of agreement other relevant papers must be sent to Green Banking and CSR Department of the central bank.

News:Bangladesh Today/27-Mar-2014