Banking

Dhaka Bank managers’ conference held

Annual Managers’ Conference for the year 2011 of Dhaka Bank Limited was held at a city hotel on Sunday.

Reshadur Rahman, chairman of the Board of Directors of the bank inaugurated the conference as the chief guest while Khondker Fazle Rashid, managing director presided over the conference, said a press release.

Among others, founder and former advisor Mirza Abbus Uddin Ahmed, former chairman ATM Hayatuzzaman Khan, vice chairman Mohammed Hanif, directors Afroza Abbas, Rakhi Das Gupta, Tahidul Hossain Chowdhury, and G M Shameem Hussain were present.

Deputy managing directors Tanweer Rahim and Neaz Mohammad Khan were also present on the occasion.

News: Daily Sun /Bangladesh/18 Jan 2011

Stocks drive profits for state banks

Rejaul Karim Byron

Rejaul Karim Byron

A leading state-owned commercial bank logged 136 percent higher profit last year from its investments in the capital market alone, compared with the previous year.

Sonali Bank earned profits of Tk 177 crore in 2010 from its investments in the stockmarket, up from Tk 75 crore the previous year, its officials said. The bank's profit from other ventures increased 41 percent.

Alongside the private banks, all four state-owned commercial bank (SCB) made good profits last year, thanks to their investments in the share market.

Janata Bank made the highest profit from the stock investments, followed by Agrani, the officials of SCBs said.

A high official of Janata Bank said: “Our profit from stockmarket rose satisfactorily and we were also considerably successful in other banking businesses."

"Deposit growth and loan disbursement increased and the number of loss-making branches decreased substantially.”

The officials of the SCBs told The Daily Star that they made huge investments as institutional investors in 2010.

Sonali Bank Chairman Kazi Baharul Islam said they got a big profit from share market. Their profit from other ventures was also considerable.

Islam said he was the convener of the government reform committee for the SCBs. “We, the chairpersons and managing directors, frequently sat together and worked with a common approach. And so the SCBs made handsome profit even outside the stockmarket.”

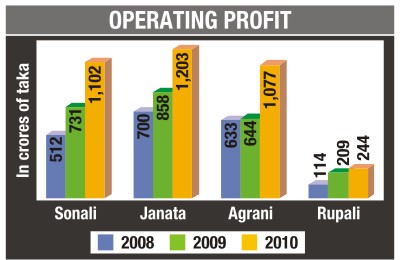

In 2010 four SCBs -- Sonali, Janata, Agrani and Rupali -- increased their average operational profit by 48 percent to Tk 3,626 crore, which was Tk 2,442 crore the previous year.

Sonali Bank's profit rose by 51 percent and stood at Tk 1,102 crore, Janata Bank's 40 percent to Tk 1,203 crore, Agrani's 67 percent to Tk 1,077 crore and Rupali's 17 percent to Tk 244 crore.

An official of Sonali Bank said the banks took rather cautious steps while investing in the capital market. We have formulated a set of rules for judicious investment in the share market holding special board meetings, he said.

In future, they will make investments in the share market after analysing the balance sheet, price-earning ratio, dividend and profitability of the company concerned.

The SCB officials said they could cut the number of loss-making branches as their overall profit went up. Sonali Bank's loss-making branches came down to 90 in 2010 from last year's 180, while Rupali Bank's loss-incurring branches came down to 22 from 58.

News: The Daily Star /Bangladesh/17 Jan 2011

SME takes centre stage

Gone are the days when budding entrepreneurs in Bangladesh stumbled to get access to funds to start their own ventures or expand existing operations. Commercial banks and many other non-banking financiers are now more than willing to facilitate their dreams with funds.

Banks and other financial institutions have been in operations in Bangladesh since its independence in 1971. But it was not until 1999 when banks paid heed to the small and medium enterprises (SMEs), which make up 75 percent of the domestic economy.

However, getting a loan is not an easy job for the first time entrepreneur. There were a number of banks in the country before the new millennium, but they were not serious about standing next to the SMEs, say entrepreneurs. They believe there have been positive changes in how banks look at them, but there is still a long way to go.

“Banks should look at the potential of an entrepreneur and make investments accordingly, rather than giving priority to their likes and dislikes,” said Abdul Mannan, owner of Remo Chemicals in Dhaka.

“Banks still only look at things like whether the borrower will be able to make regular repayments or not. This is not entrepreneur banking.”

He said small enterprises have become large over the years around the world. “We can do the same. In Bangladesh, there are many potential entrepreneurs who can do a good job. But they cannot go far for an absence of easy credit.”

“We are still talking about the cost of funds, whereas other countries have progressed far. We cannot develop in this way.”

Mannan said the banks are more interested in trading activities rather than manufacturing.

Of late, there has been a trend among the financial institutions to reach out to the SMEs. Credit goes to the central bank for this. Bangladesh Bank (BB) set targets for the financiers in 2009 for SME banking.

Local banks disbursed Tk 38,283 crore among 234,969 SMEs in the first nine months of 2010, against a target of Tk 23,995 crore. BB data shows that less than Tk 15,000 crore was lent to the sector in 2009.

In 2009, the central bank redefined SMEs and loan limits, and directed the banks to prioritise small enterprises and women entrepreneurs. The loan range for small entrepreneurs was set at Tk 50,000 to Tk 50 lakh. For the medium enterprises, no limit has been mentioned. The banks decide the amount for such entrepreneurs on the basis of need.

There are about 6 million SMEs and micro enterprises in Bangladesh, according to Asian Development Bank.

The SME is the largest sector in terms of employment generation, even though it accounts for 6 percent of the country's $100-billion economy, according to Bangladesh Economic Review 2009.

The SME sector now contributes up to 25 percent to the gross domestic product and accounts for about 40 percent of manufacturing output, 80 percent of industrial jobs and nearly 25 percent of total labour force, according to SME Foundation. Currently, banks have marked interest rates for the SMEs at between 14 and 20 percent.

Central bank officials said there is still apprehension among banks about SMEs as they do not have a clear picture of the sector and its potential.

“However, they are gradually becoming interested. Now, banks are interested for two reasons -- new business and persuasion from the central bank,” said an official of SME and Special Programmes Division of BB.

He said under the liberalised financial system, BB can not force banks to go for any particular area. “But we have been very effective in telling them what areas and segments they should cover. We have introduced some awards for the banks that comply, like easy approval of new branches.”

“As a result, many banks have come forward and are disbursing loans to the sector.”

The central bank official said banks in Bangladesh have always wanted to net large or corporate clients. “There is huge competition among banks today as there are a significant number of banks in the market. But the number of corporate houses is not that big compared to that of financial institutions.”

Banks' scope for large loans is shrinking. As a result, SMEs have emerged as a new area of business.

BB and SME Foundation are arranging a number of programmes to give banks a better understanding about the sector, to change their mindset. “But the momentum is still not there, but we are hopeful,” the official said.

SMEs face difficulties due to reluctance by banks to provide loans. Many banks are shy to lend to them because of high processing and monitoring costs.

Bankers however said banks are enthusiastic about tapping into the sector.

“We are very aggressive. Today, clients do not need to come to banks; rather our field level officers identify them and take products to them,” said Syed Faridul Islam, head of SME banking of BRAC Bank.

“SME is a major sector for growth potential for banks. We have proved that banks can still be profitable by serving SMEs. The sector has brought new growth opportunities for us,” he said.

He said: “Whenever we receive any query about loans, our officials visit them, take note of their demand and business conditions. After verifying the applicant's qualifications, we offer products.”

“Things have changed in the last three-four years, thanks to Bangladesh Bank's awareness drive,” said Islam.

BRAC Bank is the fourth largest SME bank in the world, with 429 unit offices across the country, exclusively catering to growing entrepreneurs. Today, with over 10,000 crores of loans disbursed till date, it is the country's largest SME financier.

Since its inception in 2001, it has disbursed nearly Tk 14,000 crore among three lakh entrepreneurs across the country.

Islam said interest rates for SME loans are high due to high cost of funds and monitoring.

Non-bank financial institutions also have a strong presence in SME lending.

Shafique-ul-Azam, managing director of Midas Financing Ltd, a leading non-bank financial institution, said they need a maximum of 10 days to complete a loan process.

“We need more time as we have to collect reports from Bangladesh Bank's Credit Information Bureau about the applicant on whether he or she has borrowed money from any other bank or institution.”

He said they only ask for papers that really matter. “For any businessman, we seek the trade licence, record of six month's sales and papers if he runs his business on rented house. We do not want to discourage them.”

“We even help applicants process the application, as many still find it hard just to complete the form,” he said.

Azam said his institution gives up to 5 percent rebate on interest to entrepreneurs who make timely repayment. “I think we are unique in this regard. We see banks give incentives to people who do not make payment regularly.”

Unlike many banks and non-bank financial institutions, Midas provides up to a six-month grace period to borrowers to help them generate money. “We give them time on the basis of the project. For example, a poultry farmer will not be able generate profits in the following month of a loan. In that case, we give them three-month grace period, when he will only pay interest,” Azam said.

In the last three months, Midas disbursed TK 101 crore among SMEs, taking its total loan outstanding to Tk 400 crore in the sector.

fazlur.rahman@thedailystar.net

News: The Daily Star /Bangladesh/17 Jan 2011

Fresh schemes in the offing

The central bank plans to step up its efforts to provide the much-needed financial services to the small and medium entrepreneurs (SME) across the country, officials said.

NEW GUIDELINES

Bangladesh Bank (BB) plans to update its guidelines on SME sector, prioritising a number of areas for the benefit of the entrepreneurs. BB has already published a guideline for the banks in this sector and a number of new areas will be added this year, officials said.

“In the updated guidelines, we will ask banks to keep a minimum grace period of six months to one year in case of term loans, as it takes time for the borrower-entrepreneur to generate money using the loan,” said an official.

He said a section of the entrepreneurs in the sector, like fashion houses, are keen to take loans and use them, but their business is mainly seasonal. “We will ask the banks to devise products so that such entrepreneurs can take loans three months ahead of the season e.g. the Eid, and can repay the loan at the end of the season.”

The updated version of the guidelines is due to be ready for dissemination by end February. Last year, the central bank prepared area-based plans and asked the banks grant loans in areas where a particular crop grows in abundance.

This year, BB will ask the banks to inform the central bank about their plans, the areas they want to cover and the amount of money they want to disburse, the official said.

“This will help us monitor the credit programme of the central bank.”

The new additions in the guideline will also require the banks to devise special products to cater to the needs of the growing number of women entrepreneurs.

BB also plans to look at the geographical distribution of the loans in the SME sector. “We will identify areas that receive more credits or less. It will help us broaden the credit coverage and help areas that do not get enough attention usually,” the official told the Daily Star.

CREDIT GUARANTEE SCHEME

The central bank is also planning to introduce credit guarantee scheme so that banks do not have to worry about reaching the SMEs.

Banks usually take into account the possible number of default loans while setting interest rates, which keeps the lending rates at high levels.

“If we can decrease the number of default loans through credit guarantee scheme then the banks will be eager to lend to more SMEs. But the government has to come forward to make this happen,” said a BB official.

In the past, the government introduced special schemes for small entrepreneurs. But officials said their experience was not satisfactory, as borrowers did not bother much to repay the loans, as they thought that they had taken money from the government.

On the other hand, banks also did not make efforts to recover the loans as they could easily recoup the loans from the scheme, eventually compelling the government to cancel the scheme as many borrowers defaulted on the loans.

Due to the prior unsavoury experiences, the central bank will not, this time, provide any guarantee; rather it is planning to set up a separate institution to handle the issue, the official said.

“The institution will run as a separate entity and will get premium to remain in the business. The central bank will provide the initial capital,” the BB official said.

News: The Daily Star /Bangladesh/17 Jan 2011

New DMD for Prime Bank

Md Golam Rabbani was promoted as deputy managing director of Prime Bank recently. Prior to this assignment, he was the senior executive vice president of the bank, said a statement.

Md Golam Rabbani was promoted as deputy managing director of Prime Bank recently. Prior to this assignment, he was the senior executive vice president of the bank, said a statement.

Rabbani started his career in 1977 in Bangladesh Shilpa Rin Sangstha and joined Prime Bank on October 2001.

News: The Daily Star /Bangladesh/17 Jan 2011