Default loans rise in Q3 due to tight rules

The extent of default loans increased in the third quarter due to tightening the loan classification guideline, sluggish business activities during the political uncertainty and interruption in energy supplies.

The classified loans increased by Tk44bn or 8% to Tk567bn in the July-September quarter from Tk523bn of the April-June quarter of this year, according to Bangladesh Bank data. The classified loan is about 13% of the total outstanding loan of more than Tk4tn.

The total classified loan was Tk510bn in March this year, which was Tk290bn in June, 2012.

“The classified loans increased due to tightening the guideline,” said a senior executive of Bangladesh Bank. Besides, sluggish business during the political uncertainty and lack of gas and electricity pushed the classified loans up, he said.

Bangladesh Bank Deputy Governor SK Sur Chowdhury said the commercial banks have classified the loans from March quarter following the international standard guideline issued by Bangladesh Bank.

He, however, said the banks have faced some problems to follow the new guideline. “They will overcome the problems gradually.”

According to the new guideline, banks have to classify the loans in three categories, included sub-standard, doubtful and bad or loss.

Of the total classified loans, four state-owned banks have Tk241bn, private commercial banks Tk223bn, specialised banks Tk87bn and foreign banks Tk14bn.

Of the state-owned banks, Agrani Bank’s classified loan stood at Tk51bn, which is 27% of the total outstanding loan; Janata Bank Tk47bn, which is 18% of outstanding loan; Rupali Bank Tk16bn, which is 17% of their outstanding loan; and Sonali Bank Tk125bn, which is 42% of their total outstanding loan.

Under the revised loan classification guideline, the general provision against all unclassified loans of small and medium enterprises (SME) has been set at 0.25% from the existing 1%.

Besides, the base for provisioning has been re-fixed at minimum 15% of the outstanding balance of a loan from 20%.

Under the revised provisions, the down-payment for the first time rescheduling of a term loan has been reduced to minimum 15% from at least 25% previously of the overdue installments or 10% of the total outstanding amount of a loan, whichever is lower.

The application for second time loan rescheduling will be considered upon receipt of cash payment of minimum 30% of the overdue installments or 20% of the total outstanding amount of a loan, whichever is lower.

The application for third time loan rescheduling will be considered upon receiving cash payment of minimum 50% of the overdue installments or 30% of the total outstanding amount of the loan, whichever is lower.

News:Dhaka Tribune/08-Nov-2013

‘Bangladesh a model of Islamic finance’

Financial Inclusion is a built-in concept of Islamic Finance and Bangladesh has become a role model of financial inclusion for the Islamic financial world.

Mohammad Abdul Mannan, managing director of Islami Bank Bangladesh Limited, said this while addressing the first ever ADB conference on Islamic Finance for Asia held at ADB Headquarters in Manila, Philippines recently. Organised jointly by Asian Development Bank (ADB) and Islamic Financial Services Board (IFSB), the conference was attended among others by Takehiko Nakao, president of ADB, Jashim Ahmed, secretary general of IFSB, Rajat M Nag, managing director general of ADB, Bruce Davis and Stephen P Groff, vice-presidents of ADB, Dr Ishrat husain, ex-chairman of IFSB and ex-governor of State Bank of Pakistan, Zamir Iqbal, lead investment officer of World Bank, Dr Mulya Siregar, assistant governor, Bank Indonesia and a host of experts, practitioners and regulators from ADB member countries and from the Islamic finance world, says a press release.

The conference aimed at creating greater awareness on the potentials and opportunities brought about by Islamic finance to this region and discussed the issues relating to its progress, challenges and further developments.

The conference also aimed at exploring avenues for interaction and co-operation among the members of IFSB and ADB.

Mohammad Abdul Mannan, in his presentation on “Islamic Banking: Financial Inclusion as a Core Concept: Bangladesh Experience” elaborated on the basics of Islamic Finance and Banking and shared with the audience the experience of financial inclusion in Bangladesh which is termed as the university of microfinance.

He also placed the integrated financial inclusion model of Islami Bank Bangladesh Limited based on its Rural and Urban Poor Development Schemes as a successful model that has a share of more than 50 per cent of the world Islamic microfinance, which attracted high attention of the participants in the conference.

News:The Independent/08-Nov-2013

Sonali Bank to assist other local banks to run UK services

State-owned Sonali Bank has taken an initiative to help other local banks to run their banking business in the United Kingdom, particularly the remittance service to non-resident Bangladeshis (NRBs).

Ten Bangladeshi banks were in trouble to run various businesses including remittance services after the British bank Barclays in July this year shut their accounts on ground that the banks do not match its new eligibility criteria.

“Like the Barclays, the UK branch of Sonali Bank will facilitate service to the exchange houses of different Bangladeshi banks there so they can provide their clients the services they used to deliver earlier,” Sonali Bank Managing Director and Chief Executive Officer Pradip Kumar Dutta told BSS on Thursday.

He said the exchange house of Pubali Bank already signed a consent letter with Sonali Bank for getting the services. Dutta expects that the exchange houses of other banks would also follow the suit soon because such partnership with Sonali Bank would help them provide their clients with smooth remittance services.

News: Daily Sun/08-Nov-2013

AB Bank signs MoU with CPTU on e-GP registration

AB Bank Limited signed a Memorandum of Understanding (MoU) with Central Procurement Technical Unit (CPTU), Ministry of Planning on “Registration with Electronic Government Procurement (e-GP) System” recently.

The signing ceremony took place at the Ministry of Planning at Agargaon in Dhaka, said a press release.

Under the MoU, CPTU will provide e-GP Portal Dashboard and training to nominated focal persons of the bank on e-GP portal link as the e-payment service provider.

As a member bank, AB Bank will provide services like registration/re-registration of bids/tenders and sell tender documents on behalf of procuring agencies and procuring entities within the territorial jurisdiction of the bank.

News: Daily Sun/08-Nov-2013

Shamim Ahmed Chaudhury, President and Managing Director (Current Charge) of AB Bank Limited and Amulya Kumar Debnath, Director General, CPTU, Ministry of Planning, signed the MoU on behalf of their respective sides.

Mohammad Mejbahuddin, Secretary, IMED, Ministry of Planning, Government of Bangladesh attended the MoU signing ceremony and presided over this function.

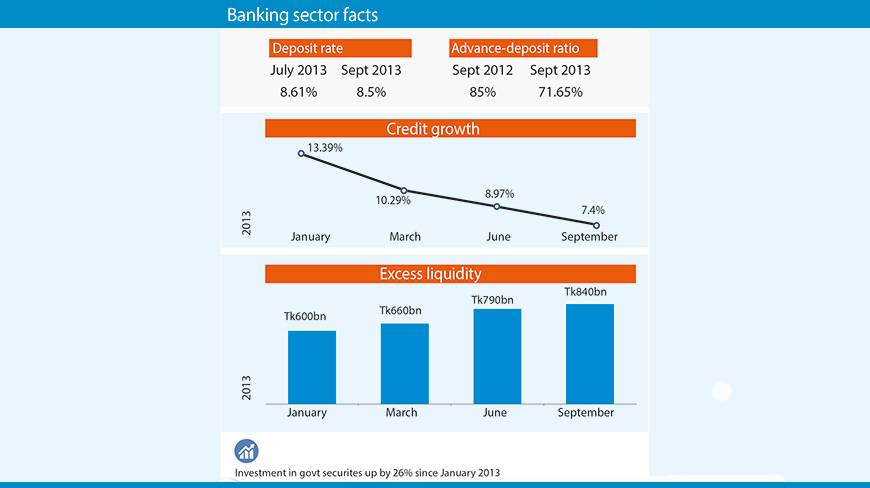

Banks burdened with excess liquidity

The country’s commercial banks are awash with idle money due to poor investment and lower credit demand, with almost all kind of business expansion remained suspended amid political uncertainty ahead of the upcoming general election.

The excess liquidity increased by Tk240bn or 40% during January-September period of the current year and stood at Tk840bn from Tk600bn in January, according to the Bangladesh Bank data.

The amount of surplus liquidity increased rapidly while credit growth dropped continuously.

The credit growth of the banks was 13.39% in January with surplus liquidity of Tk600bn, followed by 10.29% growth in March with Tk660bn in excess liquidity. The growth was 8.97% in June when the liquidity was Tk790bn and 7.40% in September as the liquidity rose to Tk840bn.

The banks burdened with the huge idle money were looking for alternative investment window as reflected from their rising investment in the government securities.

The banks’ investment in government securities increased by 26% to Tk1tn during the 9 months period till September from Tk990bn in January, according to the central bank data.

“The investment opportunities for the banks shrunk due mainly for political unrest, lack of gas and electricity. Besides, they have also barrier to invest in share market according to the amended bank company act,’’ said a senior executive of a private bank.

However, the banks were taking away investment from the capital market instead of reinvesting there as they are bound to keep their exposure limit at 25% of paid up capital and reserves, which also pushed the liquidity to go high, he said.

“As a election year, banks remained shy to disburse big loans throughout the year and in last two months, there will have no possibility to release big loans,” said National Credit and Commerce Bank Managing Director Nurul Amin.

He said credit growth also decreased due to inflow of low cost foreign loans in the private sector as provided by Bangladesh Bank.

“Banks already cut their lending rates slightly to attract the borrowers and the rate will go down further within December,” said Amin, also the President of Association of Bankers Bangladesh (ABB).

The deposit rate dropped to 8.5% in September from 8.61% in July as banks reluctant to take more public funds.

“Banks’ interest income against credit declined due to sluggish disbursement while their interest expenditure against deposit went up, adversely hitting the profit. As a result, banks cut the interest rate on deposits and also moved to reduce lending rates to stimulate credit,” said a senior executive of a private bank.

The advance-deposit ratio (ADR) in the overall banking sector also declined to 71.65% in September against 85% a year back.

The ADR is likely to go down further in the coming months, if the current sluggish trend of credit to the private sector continues and the political situation takes a turn towards further confrontational course again.

News:Dhaka Tribune/07-Nov-2013