HSBC confirms its chief holds Swiss bank account

HSBC has confirmed that its chief executive Stuart Gulliver uses a Swiss bank account to hold his bonuses.

HSBC has confirmed that its chief executive Stuart Gulliver uses a Swiss bank account to hold his bonuses.

The bank was responding to a report in the Guardian that Mr Gulliver has £5m in the account which he controls using a Panamanian company.

The bank pointed out that Mr Gulliver lives in Hong Kong and pays taxes there and has also paid any taxes required in the UK.

The statement did not mention the Panamanian company.

The details about Mr Gulliver's tax arrangements have emerged on the same day that HSBC publishes its annual results.

The Guardian article does not suggest any wrongdoing on Mr Gulliver's behalf, but it will add to the questions over HSBC's activities in the tax advisory business.

Allegations emerged earlier this month that HSBC had helped people evade UK tax using hidden HSBC accounts in Geneva.

The Financial Conduct Authority, HMRC, Swiss prosecutors and MPs on the Treasury Committee are looking into the allegations.

Last weekend the bank published an apology - signed by Stuart Gulliver - to its customers and staff adding that it had completely overhauled how it conducted its business since 2008.

Below 6pc growth not conducive to investment: Bankers

Bankers at a workshop on monetary policy yesterday said that if the GDP growth rate comes below 6 per cent, it will have psychological effect on the investors and will work as barrier to new investment in the country, reports UNB. “Below 6 per cent GDP growth will create psychological barrier to the investment,” said SA Chowdhury, former chairman of Bangladesh Krishi Bank and also former managing director of Sonali Bank Limited, told the workshop referring to the apprehensions of economists and donor agencies that the GDP growth in the country will go below 6 per cent.

The Institution of Bank Management (BIBM) organised the workshop, with its director general Toufiq Ahmed Choudhury in the chair, at its auditorium in the city.

Expressing concern, most of the speakers at the workshop apprehended that the ongoing political turmoil might affect the macroeconomic stability of the country resulting in lower GDP growth against the targeted 7.3 per cent in the current fiscal year, 2014-15.

Responding to various questions on monetary policy from mid-level bankers representing different banks, Bangladesh Bank chief economist Birupaksha Paul agreed with the idea and said that Bangladesh Bank has been trying to pursue a cautious monetary policy to achieve the growth target keeping the inflation under control.

He admitted that there is frustration among the people about the growing non-performing loan (NPL) and money laundering, which the central bank also feels sharply.

“It’s true, no central bank governor will prefer to receive award keeping its NPL high,” said the BB chief economist adding that control of everything is not in the hands of the central banks in the third-world countries.

Advocating more independence for the central bank, he said the central bank’s independence helps government maintain better coordination in implementing its programmes and policies.

Birupaksha Paul said monetary policy should be placed in Parliament and discussed by its members as it happens in many developed countries.

Former deputy governor of Bangladesh Bank Khondkar Ibrahim Khaled appreciated different aspects of the monetary policy announced by the central bank up to June this year.

Only GDP growth should not be the main indicator of development for a country like Bangladesh, he said, adding food, education and healthcare are also the areas where concentration should be given from humanitarian point of view.

Khondkar Ibrahim Khaled said money laundering must be checked and steps should be taken so that local money could be invested locally instead of flying overseas.

SA Chowdhury said private sector credit growth is falling for lack of enabling environment as a result of political instability.

“If private credit growth falls, it’ll directly hit macroeconomic stability,” he said, adding that foreign and local investment is essential for creating employment.

Expressing concern about the spillover effect of the proposed wage hike of the government employees, Chowdhury said that when this wage hike comes into effect, it would push up inflation and the private sector will be under pressure to hike their staff salaries as well.

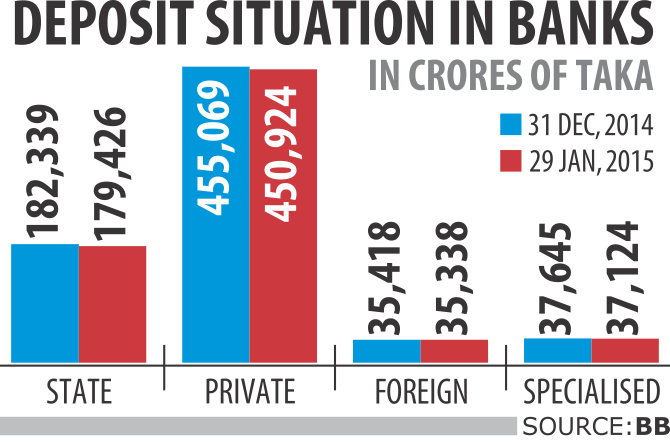

Banks' deposits fall as savers rush to savings tools

Deposits at banks dipped 1.07 percent in January from a month ago as savers rush to government savings schemes that offer higher interest rates compared to the banking system.

Total deposit at the country's 56 banks was Tk 702,814 crore as of January 29 this year, down by Tk 7,658 crore from Tk 710,472 crore in December 31 last year.

Bankers said banks have been lowering interest rates on deposits for nearly two years due to dull investment situation.

The weighted average interest rate on bank deposits was 7.32 percent in November last year, which was 8.45 percent in the same month a year ago.

Interest rates on term deposits at private banks are as high as 9.50 percent while it is 8.50 percent at state banks.

On the other hand, interest incomes on savings certificates range between 11 percent and 13.50 percent.

“So, the savers are now getting more interested in savings certificates rather than putting money in banks,” said Anis A Khan, managing director of Mutual Trust Bank.

In the five months to November of the current fiscal year, gross sales of saving instruments went up by a staggering 82 percent compared to the same period a year ago.

Banks have been sitting idle on huge piles of cash for a long time, as they could not make new investments.

Their investment situation worsened further in January because of the blockades and strikes as businesses and companies have put their borrowing plan on hold.

As a result, banks now have more liquidity in their hands and are not interested to take costly deposits, bankers said.

Khondkar Ibrahim Khaled, a former deputy governor of Bangladesh Bank, blamed the decline in banks' deposits on the seasonal effect. He said sometimes bank branches collect “hot deposits” from their existing clients in December to reach their collection target set by their head offices.

“These hot depositors can withdraw their money after December 31,” he said.

In the absence of social safety nets, the government offers higher yields on savings certificates in order to provide an income to limited-income people and elderly citizens, who are highly dependent on such sources of earning.

A number of bankers say the ongoing political unrest, which began on January 6, also hit the deposit growth.

A section of savers are withdrawing their deposits from banks to buy things, in bulk, whose prices might go up in the coming weeks amid growing uncertainty that the present situation, which has disrupted the supply chain, might linger.

There are also a section of savers who use debit cards to withdraw money from their bank accounts when needed. Savers have withdrawn large amount of money from banks, as many ATMs across the country went out of cash in January due to blockades.

The effect of such withdrawal will not be that much significant, said Khan of Mutual Trust Bank.

Bank-wise, deposits at state lenders went down by 1.59 percent in January compared to December, according to statistics from Bangladesh Bank.

The fall is 0.90 percent at private banks, 0.22 percent at foreign banks and 1.38 percent at state-run specialised banks.

The decline in the specialised banks was caused largely by the 3.18 percent decrease in deposit growth at scam-hit BASIC Bank.

Year-on-year deposit growth also slowed in January. It was 12.58 percent in January 29 this year, which was 13.26 percent in December 31 last year.

News:The daily Star/23-Feb-2015New banks go for risky lending

New banks are lending out heavily -- 70 to 80 percent of their total loans -- to corporate clients instead of small and medium enterprises and retail consumers, insiders and analysts said.

The risk is: if a big client fails to pay back in time, the bank may suffer as it may not be able to make adequate provision from its small profit.

“Directors want quick profits, which is very unlikely for a new bank,” said the chief executive of a new bank, seeking anonymity. “It takes at least three to five years to generate sustainable profits and pay dividends.” Nine new banks that came to the market amid political unrest in the second half of 2013 are struggling to do business at present, facing intense competition from 47 old banks in lending and attracting deposits.

Lending out is the biggest challenge for a new bank, as borrowers demand the lowest interest rate without considering the banks' cost of funds.

According to these banks, the cost of their funds is between 11 percent and 12 percent, which is well within a single digit for many old banks. In terms of lending, if a new bank offers a borrower 11 percent, an old bank offers 10.5 percent.

“Depositors have high expectations from us, while borrowers want the lowest rate in the market. We are in a double bind,” said Rafiqul Islam, managing director of South Bangla Agriculture and Commerce Bank (SBAC).

Moreover, businesses are passing bad times and it has become impossible to get a good client, who wants to set up new factories or expand the existing ones amid an ongoing anti-business climate, Islam added. SBAC has lent out Tk 1,363 crore in 2014, coming in third among the new banks, after Union Bank with Tk 2,828 crore and NRB Commercial Bank with Tk 1,441 crore.

SBAC booked Tk 32 crore in operating profit and the net profit would be less than Tk 20 crore, which is a tiny figure to pay dividends against Tk 400 crore in capital.

“We need more time, around two years, to pay dividends to our shareholders,” said the SBAC chief executive.

To make their directors happy, some banks are lending aggressively to corporate clients that may end up as bad loans.

Union, NRB Commercial, SBAC and NRB Global went for aggressive banking, their lending data shows.

“Around 80 percent of our loans have gone to corporate clients,” said an official of Union Bank. It is tough for a new bank to lend out Tk 100 crore, especially to small businesses, he said, adding that strict monitoring is also needed to recover the money from small borrowers.

Muklesur Rahman, managing director of NRB Bank, said, “We are doing progressive banking, not aggressive, to make us sustainable. We have to keep in mind that we do business with depositors' money.” NRB lent out Tk 620 crore until December 2014.

Modhumoti Bank looks more cautious among the nine entrants. It lent out only Tk 413 crore until the end of 2014.

Salehuddin Ahmed, a former central bank governor, said he had always opposed issuing licences to new banks during his tenure till May 2009 as the country and the economy do not need any new banks.

“Many of these new banks have no sustainable and long-term business vision. Many sponsors of these banks do not even understand the banking business,” Ahmed said.

“That's the reason why the directors of these new banks want profit in one or two years.”

New banks could create entrepreneurs by funding SMEs and other productive sectors, he said.

News:The Daily Star/23-Feb-2015ONE Bank Limited

ONE Bank Limited signed a memorandum of understanding (MoU) with Grand Sultan Tea Resort & Golf Resort, Srimongal recently. Head of Retail Banking of the bank Gazi Yar Mohammed and Head of Sales & Marketing of Grand Sultan Tea Resort & Golf Md Sayedul Islam Bhuiyan signed the MoU on behalf of their respective organisations. Under the MoU, OBL credit cardholders and OBL employees will enjoy up to 55 per cent discount on rack room rents upon exhibiting their respective credit cards or employees ID card.

ONE Bank Limited signed a memorandum of understanding (MoU) with Grand Sultan Tea Resort & Golf Resort, Srimongal recently. Head of Retail Banking of the bank Gazi Yar Mohammed and Head of Sales & Marketing of Grand Sultan Tea Resort & Golf Md Sayedul Islam Bhuiyan signed the MoU on behalf of their respective organisations. Under the MoU, OBL credit cardholders and OBL employees will enjoy up to 55 per cent discount on rack room rents upon exhibiting their respective credit cards or employees ID card.