Banking

Bank Asia signs online payment deal with AlertPay

Bank Asia has signed an online payment gateway service agreement with Canada-based AlertPay, a press release said.Through this deal, Bank Asia became the first Bank in Bangladesh to establish business through Online Payment Gateway Service Providers (OPGSP) to provide service to the indivudual service exporters of Bangladesh.

Casada Technology will work as the local agent for AlertPay here in Bangladesh. AlertPay is an established OPGSP, who offers a flexible way to send and receive money worldwide through Online Payment Gateway Service.

The government recently permitted instant money transfer facilities to service exports as Bangladesh is becoming a service exporting country, especially in software sector, which involves small value exports in such as data entry and software.

Mehmood Husain, managing director, Irteza Reza Chowdhury, deputy managing director of Bank Asia, and Firoz Patel, chief executive of AlertPay, signed the agreeent on behalf of the respective sides. Intezar Ahmed, chairman of Casada Technology, was also present.

The Independent/Bangladesh/ 29th Dec 2011

Borrowing from banks hampers sector’s growth

The managing director of Shahjalal Islami Bank, Abdur Rahman Sharker has observed that despite global economic recession, poor infrastructure and volatile capital market, the banking sector of Bangladesh has been performing well.

In an exclusive interview with the Independent, he however, pointed out that default culture, intensive competition, vulnerable capital market, government borrowing from banking sector, absence of secondary market for treasury bill/bond hampered the growth of banking sector.

Excerpts:How do you observe the performance of banking sector in the country?Up to September 2011 total deposit (excluding interbank and govt deposit) reached 3,959,420 million Taka whereas total deposit at the end of December 2010 was 3,461,377 million Taka that is 14.39% growth over December 2010.

Bank Credit increased by 14.33% to 4,342,849 million taka in September 2011 from 3,798,439 million Taka in December 2011. However, due to increase of Government borrowing, among the component of Bank credit, exceptional growth was found in Bank Investment (29.29%). Except income from capital market service, most of the banks able to secured tremendous growth of profit in others areas of its operation like net interest income, commission, exchange, other investment income etc.

Despite global economic rescission, infrastructure shortage, volatility of capital market, banking sectors of Bangladesh are performing well. What are the areas of your bank working ?We work in every areas of banking operation like deposit mobilization, investment, export/import business, foreign remittance, guarantee business etc.

We are present in every sector of business/industries like, readymade garment, textile, energy, transport, water and sanitation, environment, rural development education, social protection and health, science and technology, financial markets, agriculture, SME, automobiles, steel, chemicals, and pharmaceuticals etc.What are the new services in your bank?

This year we have introduced school banking, off-shore banking, women entrepreneur finance, agro finance etc.Do you think there is any necessity of new banks? There is no denying the fact that the financial system plays a significant role in the economic development of a country.

The importance of an efficient financial sector lies in the fact that it ensures domestic resources mobilisation, generation of savings, and investments in productive sectors. In fact, it is the system by which a country’s most profitable and efficient projects are systematically and continuously directed to the most productive sources of future growth.

Moreover, we know that a significant percentage of rural population is not covered by banking sector, Unauthorised money collecting and lending organisations deceive them. However, Bangladesh Bank should have comprehensive research about the requirement of more banks in the light of long term GDP growth, long term monetary policy and other economic and social factors.

Bangladesh Bank also has clear guidelines for setting up new bank as well as merger and liquidation of the weak bank. Political considerations should not be given importance while awarding license for new bank.What is the overall performance of your Bank?Despite liquidity crunch, capital market volatility, we have been able to achieve deposit growth by 25.44%, investment growth by 25%.

Our capital adequacy ratio is 10.65% which is above the requirement of 10% as per Basel-II. This year we are going to open 10 new branches. Our income from core banking business significantly increased from that of previous years. What is the target for current and next year?Current year is already nearing its end.

In the next year we have plans to expand our business and to increase our branch network throughout the country, we have also plans to set-up more ATM booths, introduce new deposit and investment products specially for SME and agro based products and mobile banking to include the segment of rural people outside bank coverage.

Who are the main targets of your loan disbursement projects?In Bangladesh, demand for loan product is dominated by corporate clients. However, we are taking initiatives to expand credit in SME, agriculture, and women entrepreneur sectors covering the need of rural people providing financial services.

How do you evaluate the overall condition of your bank?Strong capital base, quality assets (very low default investment), prudent and efficient management team, professional dedicated board members, remarkable growth of deposit, investment, profit, diversified customer base bring the bank in strong footing among the third general banks in Bangladesh.

What do you think about reaching out to the banking services to those not covered by banking sector ? People living at the base of the pyramid are typically “unbanked,” meaning they do not have bank accounts and cannot access related financial services, such as consumer credit, home mortgages, or business loans.

SJIBL is working with businesses and entrepreneurs to introduce new tools and payment systems that enable low-income people to gain access to quality banking services, as well as income-generating opportunities. SJIBL is pioneering new directions for companies to use micro-credits as a vehicle to bring innovative solutions to the pressing needs of the majority.

We are emphasising, opening of more branches (agri/SME branch) to rural ‘unbanked’ areas of the country.What about the banking services in the villages? How many branches of your banks are located in the village areas?There is no doubt that a significant percentage of village people is ‘unbanked’ and we are trying our best to reach village people. At present we have 22 rural branches out of 63 branches.

This year we got license for 3 more rural branches. Do you want to introduce mobile banking, if yes, then when and how?Yes, we are actively working on it and hopefully by 2012 we will introduce mobile banking.What is your future plan and programme to expand your service and network?In future, we have plans to diversify our service throughout the country through introduction of new, innovative deposit and investment product, ATM service, mobile banking, full fledged online banking, priority banking etc. What about the default loan culture?

What are the remedial measures you suggest?Persistent loan defaults has become the order of the day in developing countries. There has been hardly any bank or financial institutions in developing countries which has not experienced persistent loan default. Loan defaults occur when borrowers are not willing or able to repay loans. Loan defaults are one of the critical problems in banking industry in Bangladesh.

Following may reduce default loan culture:1. Awareness among the borrower that bank deals with public money which should be repaid in time.2. Strengthen and ensure internal control mechanism.3. Formation of loan workout department or problem loan handling department in the individual banks.

4. Keeping bank free from all sorts of influences and rationalising and increasing the efficiency of the manpower5. Rescheduling should not be allowed for more than two times.6. Quicken legal process7. Ensuring effective supervision of Bangladesh Bank by increasing the efficiency of human recourses.8. Extending cooperation to loan defaulters by the administration should be stopped.

9. Ensuring ethical standard and effective cooperation among bankers, legal advisers and court as well.10. Finding out means for stopping frequent stay-orders by the courts11. Making provisions to allow only large loans to make writ applications to special bench of High Court.

12. Providing severe punishment to corrupt bankers.How do you evaluate the overall banking sector compared to the banking on global perspective?Compared to global perspective, banking sector of Bangladesh is more resilient to risk, because of its capital structure (significant portion of capital are Tier-I-crore capital), Bangladesh Bank’s strong vigilance, absence of derivative products, diversification of products, insignificant exposure to foreign market, strong remittance inflows, commitment to fulfill its social responsibilities, strong customer base, growing market, in-house practice of corporate governance etc..

However, default culture, intensive competition, vulnerable capital market, government borrowing from banking sector, absence of secondary market for treasury bill/bond hampered the growth of banking sector.

The Independent/Bangladesh/ 29th Dec 2011

A challenging year for banks

Banks in Bangladesh passed a critical year, surfing through an anti-business climate both at home and abroad in 2011.

Amid challenges, the banking industry witnessed a major change -- deregulation in some major areas including the interest rate and exchange rate, in the outgoing year.

Soaring inflation, huge bank borrowing by the government, sliding foreign investment, aid and remittances, a bearish stockmarket and lack of infrastructure were the main barriers at the local level that out banks in a tight spot.

A shift in imports -- from food grains to fuel oils and fertilisers -- also affected banks' businesses in the outgoing year. However, the liquidity crisis was the most discussed issue in 2011.

On the international front, the ongoing sovereign debt crisis in Europe, which is a major destination for Bangladesh's exports, and the troubled US economy, also hit local businesses.

“A lot of non-bank factors affected our business in 2011,” said Nurul Amin, managing director of NCC Bank. “The overall business climate, both domestic and global, was not favourable for banks.”

“There was a liquidity pressure, but not a crisis,” remarked Helal Ahmed Chowdhury, managing director of Pubali Bank, the largest private bank in terms of network, on the outgoing year.

After hefty profits in 2009 and 2010, driven by a surge in investment demand and whooping gains from capital market operations, banks felt the pinch in 2011, especially from the second quarter, and expected a slowdown in growth.

“Banks will not post healthy growth this year,” said Amin of NCC Bank, also the chairman of the Association of Bankers Bangladesh, a forum of private bank chief executive officers.

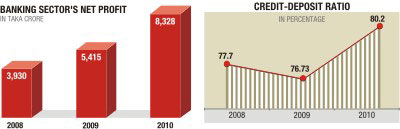

Bank operating and net profits surged in 2010, riding on gains from the stockmarket and a rebound in investment demand after two years' of sluggishness when the caretaker government was in power in 2007-08.

The banking sector's operating profits rose by over 47 percent to Tk 17,092 crore in 2010 from Tk 11,625 crore a year ago. Net profits also increased by nearly 54 percent to Tk 8,328 crore in 2010 from Tk 5,415 crore in the previous year.

The industry's return on assets (ROA) and return on equity (ROE) also increased alongside net profits. In 2010, the ROA increased by 34 basis points to reach 1.72 percent, while the ROE increased by 3 basis points in 2010 to reach 19.89 percent.

“Banks' investment opportunities were limited in 2011 due to a gas crisis. The housing sector and all consumer credit were also squeezed in the outgoing year,” said Touhidul Alam Khan, head of corporate affairs of Bank Asia.

Banks faced a lot of other challenges as well, of which, asset-liability management, deposit mobilisation, managing interest rates after withdrawal of the cap and declining remittance and volatility in the exchange rate were the major ones.

Banks overextended lending to make profits that created the asset-liability mismanagement situation in 2011, bankers said.

“Some banks tried to destabilise the market by distorting treasury management,” said Chowdhury of Pubali Bank.

Despite these challenges, banks tried to diversify lending to potential areas, said the corporate affairs chief of Bank Asia.

Power, construction and shipbuilding are some new avenues where banks invested in the outgoing year, Khan added.

“Managing the asset-liability issue was the biggest challenge in the outgoing year. But this will remain a big challenge in the coming year, following the requirements of Basel-II,” said Khan.

Banks have to be more cautious in their investments, he pointed out.

Even though 2011 was a challenging year for banks, they did get some freedom.

Banks got a decontrolled interest rate and liberalised norms for foreign exchange. Earlier, the central bank imposed a ceiling on the lending rate and intervened in the foreign exchange market frequently.

In 2011, Bangladesh Bank (BB) withdrew the cap on the lending rate that was imposed at different times to support the country's business sector. Now banks are competing with each other and offering good rates to grab customers.

Though lending rates are still competitive, exchange rate became volatile soon after the central bank kept itself away from intervention as in previous years.

In 2011, the taka depreciated by 15 percent and reached Tk 82 in exchange for a dollar at import levels.

“BB did not deregulate us. Rather it was a self-regulation,” said Amin, chairman of the bankers association.

“We had freedom, but the central bank monitored our activities efficiently,” said Chowdhury of Pubali Bank.

The Daily Star/Bangladesh/ 29th Dec 2011

Eurozone banks park record amount of funds at ECB

Eurozone banks deposited a record amount of overnight funds at the European Central Bank on Monday, official data showed Tuesday as banks remain extremely wary of lending to each other.

Banks put 411.8 billion euros ($535 billion) on deposit for 24 hours at the European Central Bank, beating the previous record of 384.3 billion euros seen in June 2010. The level of deposits at the ECB bank is an indicator of the reluctance of banks to lend to each other on the pivotal interbank market.

The money deposited earns an interest rate of 0.25 per cent, which is less than the rate available on the interbank market.Banks become reluctant to lend to each other notably when they are concerned about the capacity of the borrower to repay the loan.

Last week, 523 banks borrowed a record 489.2 billion euros from the ECB in a brand-new three-year lending facility, a move which the European Systemic Risk Board said would ease funding pressures on banks. The ECB agreed to make the cash available so as to avert a possible credit crunch, charging just 1.0 per cent interest.But the deposit data suggest the banks are now simply parking the cash with the ECB.

The Daily Independent/Bangladesh/ 26th Dec 2011

RAKUB holds cabinet meeting

RAKUB organised the cabinet meeting on Monday.

The cabinet has approved a subsidiary company of RAKUB entitled ‘RAKUB SME Financing Company Limited’ with a proposed capital of taka 5,000 million( 500 crore) with a paid up capital of taka 350 million, says a press release.

The company will be governed by a five-member board of directors. It is learnt, under the financial assistance of Norwegian government, the loan disbursement programme under the Small Entrepreneur Credit Programme started in 2002-2003.

Presently, the programme is being conducted through RAKUB branches of 40 upazilas of eight districts. After turning the project into a company, not only the small entrepreneurs but also medium entrepreneurs will get the loan facilities.

The Daily Independent/Bangladesh/ 28th Dec 2011