Al-Arafah Bank hands over blankets to BB

.jpg) AFM Asaduzzaman, General Manager, Bangladesh Bank, receives the blankets from Kazi Towhidul Alam, Deputy Managing Director, Al-Arafah Islami Bank Limited at a function in Dhaka recently.

AFM Asaduzzaman, General Manager, Bangladesh Bank, receives the blankets from Kazi Towhidul Alam, Deputy Managing Director, Al-Arafah Islami Bank Limited at a function in Dhaka recently.

Al-Arafah Islami Bank Limited handed over blankets to Bangladesh Bank for distributing among the cold-affected people across the country.

AFM Asaduzzaman, General Manager, Bangladesh Bank, received the blankets from Kazi Towhidul Alam, Deputy Managing Director, Al-Arafah Islami Bank Limited recently.

Jalal Ahmed, Assistant Vice President of the bank was present on the occasion.

Al-Arafah Islami Bank Limited is providing more than 5 thousand blankets to the poor of 23 districts of the country.

SJIBL holds annual managers’ conference

Shahjalal Islami Bank Limited (SJIBL) organised a two-day annual managers’ conference at Ruposhi Bangla Hotel in Dhaka on Friday.

Farman R Chowdhury, Managing Director of the bank, presided over the conference, said a press release.

AK Azad, Chairman of the board of directors of the bank, attended the function as chief guest.

The meeting evaluated the performance of the bank during last year and adopted necessary strategy and action plan to achieve the target for the remaining time of the year.

No vault can provide you absolute protection

n recent days we have observed some concerns on vault security. Vaults of some banks are successfully attacked by bank robbers. This created a scope to discuss certain things about vault security which many of us are ignorant.

First thing we need to understand that no vault can provide you absolute protection. It can sustain attacks for a specific period of time as per their rating. Therefore a vault needs to provide protection from fire or attacks of bank robbers for desired period of time within which a spate mechanism must be activated to detect the attack and response appropriately. In western country there are organizations which test vault and provide rating. For example there is a testing company named ‘Underwriters Laboratory” (UL) who basically rates various types of safe and vault and label them accordingly.

Typically vaults are situated at or below ground level so they do not add to the stresses of the structure housing them. If a vault must be built on the upper stories of a building, additional care must be taken to avoid building collapse which should be designed by proper architect. Doors of such vaults are normally 6 inch thick, and they may be as much as 24 inches thick where for better protection. Because these doors present a formidable obstacle to any criminal, an attack will usually be directed at the walls, ceiling, or floor, which must for that reason match the strength of the door. As a rule, these surfaces should be twice as thick as the door and never less than 12 inches thick.

If possible a vault should be surrounded by narrow corridorsthat will permit inspection of the exterior wall of the vault but the corridor will be sufficiently narrow to discourage the use of heavy drilling or cutting equipment by attackers. It is important that there are no power outlets anywhere in the close vicinity of the vault; such outlet may help the attacker to use their tools against the vault.

In a vault room there are practices to keep safes which are generally of two types; Record safes and money safes. Record safes are designed as fire resistant while money safes are burglar resistant. A record safe with an underwriter laboratory (UL) rating of 350-4 can withstand exterior temperature building to 2000*F for 4 hours without permitting the interior temperature to rise above 350*F.

Burglar resistant safes are nothing more than very heavy metal boxes without wheels, which offer varying degrees of protection against many forms of attack. A safe having weight of 750 pound with a UL rating of TL 15 means, it can withstand attack by hand tool for only 15 minutes. Likewise there are different types of rating like TRTL 30 means the safe can withstand attacks by torch and tool for 30 minutes. A safe less than 750 pounds of weight must be chained with the floor wall.

As per underwriter laboratory rating vaults are classified as UL 1, UL 2 , UL 3. UL 1 generally provide protection for 30 minutes while UL 2 provides 1 hour and UL 3 provides 2 hours of protection from a dedicated attackers who are using torch, tools, explosives and modern cutting materials.

One must understand that a vault its cannot provide protection from dedicated and determined attackers for a prolonged period of time. Therefore a security counter measure deign, target hardening, crime prevention through environmental design (CPTED), proper alarm system, proper CCTV system, proper security policy and procedures and proper response mechanism need to be integrated to keep a vault safe from a dedicated attackers.

News:Dhaka Tribune/01-Feb-2014

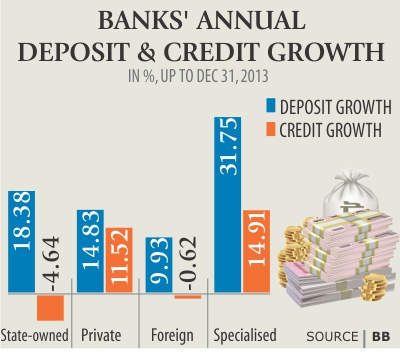

Banks struggle as loan appetite diminishes

Banks are facing a huge mismatch between credit and deposit growth, which has not only affected their profitability but also hurt savers.

In 2013, bank deposits grew 16.26 percent and credit only 7.41 percent from a year ago, according to central bank statistics.

Though the banks' deposits increased, they are unable to invest the money, leaving them with excess liquidity of around Tk 90,170 crore on December 31, 2013. Subsequently, both the deposit and lending rates were slashed.

On average, the deposit and lending rates last December stood at 8.39 percent and 13.45 percent respectively in contrast to 8.47 percent and 13.8 percent a year ago.

As the deposits could not be invested, most of the banks have lowered the interest rate on them, a bank official said, adding that the rate of interest on term deposit in most of the banks is a maximum of 11 percent, which was more than 13 percent even a few months ago.

The state-owned banks, which have cut their rate of interest more than the private banks, have discontinued various deposit schemes using various excuses to check their losses.

Zaid Bakht, research director of Bangladesh Institute of Development Studies (BIDS), said the investment demand was low for the last two years, but political unrest in the closing months of 2013 compounded it.

Bakht, who is also a director at Sonali Bank, the largest state-owned bank, said they are not getting any application for term loans of late, while the demand for trade financing has also decreased.

The scams unearthed in the banking sector in 2012 had a lingering effect, prompting officials to exercise greater caution when giving out loans, he said.

Moreover, the higher-ups have taken off the authority from the lower echelons of the banks to grant loans.

To recover the losses from the idle deposit, the banks have been investing in the treasury bills and in the call money market, but the interest rate there has been low as well.

Subsequently, the Sonali Bank board has now urged the management to set targets for the bank branches, in a bid to speed up disbursement.

Bakht also said the bank management has been asked to quickly process the good loan proposals.

In the first quarter of the fiscal year, industrial term loan disbursement dropped 8.64 percent year-on-year, while trade financing 12.9 percent, according to central bank statistics.

Meanwhile, the monetary policy statement for the second half of the fiscal year released on Monday said the credit decline is partly due to sluggish investment demand in the lead-up to national elections, tighter lending practice by banks as well as the fact that there are two new channels through which entrepreneurs can excess overseas lenders who offer lower cost financing.

One existing channel is borrowing by companies for term-credit purposes, with most having a maturity beyond five years—around $534 million was approved in first six months of the fiscal year, which was $1.82 billion last fiscal year and $1 billion in fiscal 2011-12.

In addition, private capital flows to local companies have also grown due to the addition of short-term foreign currency loans for working capital purposes in the form of 'buyers credit' and 'discounted export bills'.

Lending rates have fallen faster than deposit rates, Bangladesh Bank said in its monetary policy statement. Domestic lending rates have fallen due to lower costs of funds for banks, lower demand for credit as well as due to increasing competition from overseas lenders whose lending rates are in single digits, it added.

News:The Daily Star/01-Feb-2014

DBL opens branch in Narayanganj

Dhaka Bank Limited (DBL) opened its 72nd branch at Araihazar in Narayanganj on Thursday.

ATM Hayatuzzaman Khan, former chairman and sponsor shareholder of the bank, inaugurated the branch as chief guest, said a press release.

Abdul Hai Sarker, Chairman and founder chairman of the bank, Nazrul Islam Babu, MP, Abdullah Al Ahsan, Director, Syed Abu Naser Bukhtear Ahmed, Independent Director, Khondker Fazle Rashid, Managing Director, Emranul Huq and Khan Shahadat Hossain, Deputy Managing Directors, Arham Masudul Huq, Company Secretary and SEVP, Branch Manager, and executives of the bank attended the function.

News:Daily Sun/01-Feb-2014