Non-banks on a more stable financial keel than banks

Non-bank financial institutions' default loans did not increase as much as banks in the first six months due to low volumes of loan portfolio.

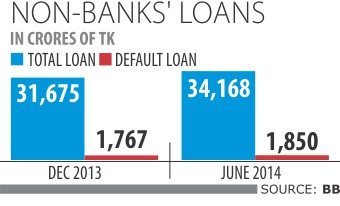

Between December 31 last year and June 30 this year, the NBFIs' default loans increased 4.69 percent in contrast to banks' 26 percent.

At the end of June, their default loans stood at Tk 1,850 crore, which is 5.4 percent of their total credit. On December 31 last year, defaults amounted to Tk 1,767 crore, 5.58 percent of their total credit.

Bank officials said the default loans of the NBFIs increased at a lower rate as their loan volume is smaller than banks'. On June 30, the total outstanding loans of banks stood at Tk 34,168 crore, 8.5 percent of their total advances.

Of the 30 NBFIs, 10 had default loans upwards of 10 percent.

Asad Khan, chairman of the Bangladesh Leasing and Finance Companies Association, said though bad loans of NBFIs increased slightly, it is much better than that of banks.

“We have seen nothing like the recent scams in banks in issuing loans in the NBFI sector.”

Khan, also the managing director of Prime Finance and Investment Ltd, said the NBFIs were cautious in disbursing loans, keeping their default rates low.

He, however, expressed concern about the narrowing of the playing field for the financial sector in general. At present, 56 banks and 31 NBFIs operate in the country.

While the number of institutions has increased, business has not increased proportionately, according to the Prime Finance MD.

Meanwhile, owing to their default loan portfolio, the NBFIs' capital position is improving by the day. Last year, the NBFIs' capital base increased 17.7 percent year-on-year to Tk 7,280 crore.

“The trend of increasing capital shows the moderately sound financial base of NBFIs,” said the central bank's Financial Stability Report published last week.

In 2013, the NBFIs' total operating profit increased 47 percent to Tk 1,660 crore.

The major funding sources of NBFIs are: capital, term deposits, credit facilities from banks and other NBFIs, call money, bonds and securitisation.

NBFIs are allowed to mobilise term deposits only with tenure no less than six months. Banks also invest in bonds/debentures issued by NBFIs, which is another source of funds.

The loans disbursed by the NBFIs though are concentrated in a few sectors.

Around 15 percent of the loans extended by NBFIs went to trade and commerce, 12 percent to power, gas, water and sanitary service, 12 percent to housing and 9 percent to garment and textile sector, according to the central bank report.

News:The Daily Star/7-Sep-2014

Comments