Interest rate spread rises above 5%

The interest rate spread crossed again the desired level of 5% - only after two months it stayed below the level.

The gap between average lending and deposit rates of 55 commercial and specialised banks went up to 5.06% in December last from 4.97% in November and 4.95% in October, after coming down from 5.01% in September last year, according to latest Bangladesh Bank figures.

“The excess liquidity in the money market did not help much in reducing the lending rates,” said a senior official of Bangladesh Bank.

Bankers, however, argued that the banks having high administrative cost could not reduce the spread.

Twenty three commercial and specialised banks have failed to bring down interest rate spread to the level as Bangladesh Bank desires.

They were maintaining returns at higher rates despite majority of the 55 banks operating in the country reduced the lending rates, contributing to push down the overall spread below the level.

Bankers, however, disagreed with the method of calculating the spread as they requested the central bank to set a definition in accordance with the reality.

They said the present spread does not reflect the true picture as the definition has not been set yet.

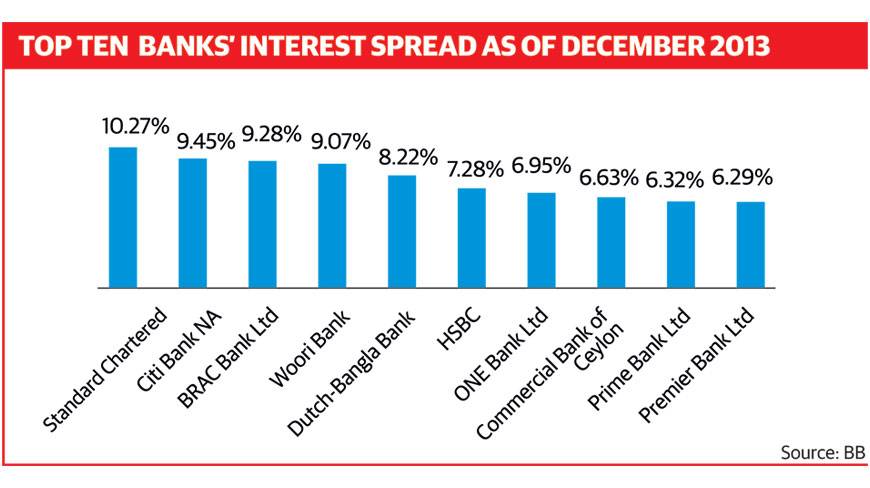

Among the private commercial banks, BRAC Bank maintains highest spread of 9.28% and, among the foreign banks, Standard Chartered has the highest at 10.27%.

Bangladesh Development Bank maintains the lowest spread of negative 0.45%, followed by NRB Bank, one of the new banks, which has 0.47% spread. Among the state-owned banks, Rupali Bank has the highest spread of 5.34%.

Among the 39 private commercial banks, the spread in 16 are still above 5%. Among the nine foreign commercial banks, the spread in six is above the limit. These are: Standard Chartered Bank, Habib Bank, Citibank NA, Commercial Bank of Ceylone, Woori Bank and HSBC.

Managing Director and Chief Executive Officer of Eastern Bank Limited Ali Reza Iftekhar said the present spread scenario does not reflect the true picture as the definition of spread is yet to be set.

“We have already talked with the central bank several times to make it up and the central bank has agreed to set a new definition in line with the reality,” he said.

However, both the lending and deposit rates are gradually coming down, as “we are cutting down the rates, said Iftekhar, also the chairman of Association of Bankers Bangladesh (ABB).

Most of the banks have already brought down their average lending rate due to lower credit demand caused by the recent political turmoil. They also lowered the spread by cutting the deposit rate.

However, many banks have failed to bring down the spread because of their higher administrative cost.

A banker said the central bank does not consider the return on other investments like government securities, but it is now calculating net interest margin to gauge spread.

He said the banks generally compute their spread as the difference between their cost of funds and return on investment, generally known as earnings.

News:Dhaka Tribune/13-Feb-2014

Other Posts

- BRAC Bank to give Tk 780m to Envoy Textile

- Business feared to be deprived of BB loan

- Bank branches in 83 upazilas remain open tomorrow

- Debt servicing becomes expensive

- Rural savers’ bank to start journey from July

- ONE Bank signs deal with Corolla Corporation

- NCC Bank signs MoU with DIU

- Prime Bank holds orientation

Comments